This post may contain affiliate links. Please read my disclosure for more info.

Were you ever taught how to set up a personal budget? For something that has such a major effect on our lives, ie, financial stability, we’re taught precious little about the basics. Or, even if we’re given some guidance early on, it just seems to come at the wrong time and we’re not ready to hear it!

So, in this post, I’m going to spend some time talking about how to set up a personal budget, pinpoint some of the pitfalls you may encounter and also give you some personal budgeting tips. You can also download my free Basic Budget Worksheet so that you can put what you learn into practice immediately.

How To Set Up A Personal Budget

Spending a little time gathering together the tools and information you need before diving into the worksheet will make the task easier and most likely the outcome more accurate. Although, if you’ve never set up a personal budget before, don’t be put off by the idea of perfect accuracy as I can guarantee that there will be something you’ll forget to include. This happens to all of us!

Step 1 – The Basic Tools and Information for Preparing a Personal Budget

• Bank statements (1 month minimum, 3 months is a bonus : ) )

• Credit card or loan payment schedules (you may be able to get this information on your bank statement)

• Pens or pencils (your preferred choice)

• Calculator

• Notebook or scrap paper

• Quiet time 🙂

Before you start the next task, decide whether you want to set up a weekly or monthly budget. But even if you decide to set a weekly budget, I’d suggest you still run through a whole month’s worth of statements.

Step 2 – Capture Your Income Patterns

Using your notebook and bank statements, work your way through each statement page making a note of all the income sources. Note the following:

• Name of company/organisation who paid into your account

• Method of payment (directly paid in; cash paid in; cheque paid in etc)

• The amount

• Frequency (daily; weekly; monthly; variable)

Make a few notes as you go along to identify regular, ongoing income and one-offs that you’re not likely to receive again (or only intermittently).

Step 3 – Capture Your Expenditure Patterns

You are likely to have far more entries on your statements for expenditure than income, so this task will take a little longer. However, this part of the process will give you the insights you need so that you can see where your money is going!

So once again, using your notebook and bank statements, work through each page making a note of all your expenditure, but this time grouping them by category so that you arrive at a weekly or monthly total for each category. Here’s an example:

• Groceries 49.88 + 27.13 + 12.00 + 55.81 + 12.85 = 157.67 (total)

• Fuel 25.00 + 23.50 + 25.00 = 73.50 (total)

• Rent 150.00 = 150.00 (total, once per month)

• Unknowns! 10.00 + 4.50 + 25.00 + 30.00 = 69.50 (total)

Keep doing this until you have a complete list. But, don’t get too hung up on the categories at this stage, the important thing is to get the information together. Keep the categories meaningful for yourself and remember no one’s watching or judging!

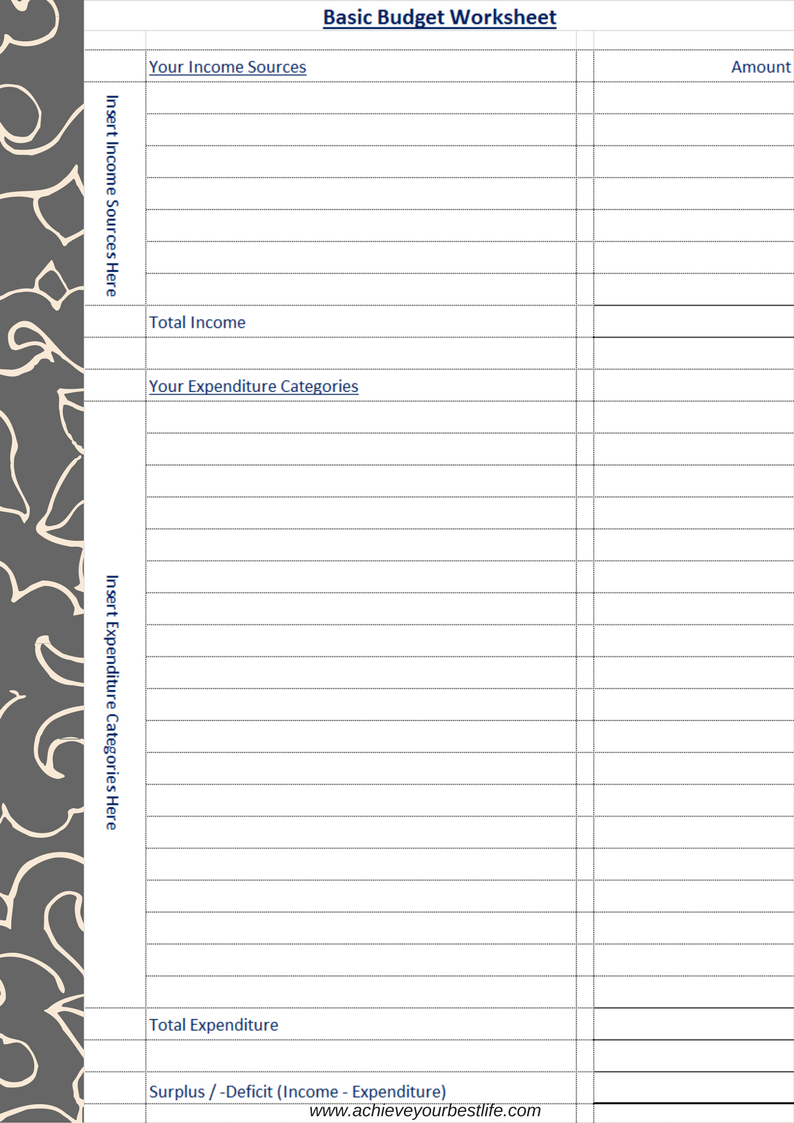

Step 4 – Transfer Income Information to the ‘Basic Budget Worksheet’

1. Using the Basic Budget Worksheet, take the information you have about your income and enter your known regular income into the top part of the Worksheet.

2. ‘Sense’ check the numbers. In other words, if you know you’re not going to receive a particular income source or if you know it’s going to change, remove or change it now.

3. Once you’ve done the above, total all the income.

Step 5 – Transfer Expenditure Information to the ‘Basic Budget Worksheet’

Repeat the process for your expenditure:

1. Using the Basic Budget Worksheet, take the information you have about your expenditure and enter your known regular expenditure into the bottom part of the Worksheet.

2. ‘Sense’ check the numbers. In other words, if you know you spent less on groceries this month because you were away, then increase your groceries budget to a sensible level.

3. Once you’ve done the above, total all the expenditure.

Step 6 – Have you got a surplus or a deficit?

The final step in the Worksheet is to fill in the Surplus/Deficit box at the bottom of the Worksheet.

Take your total income and deduct your total expenditure. If it’s a positive figure you have a surplus, if it’s a minus figure you have a deficit.

Step 7 – What to do Now

If you have a surplus, congratulations, you are living within your means! After doing a careful check of your income and expenditure numbers, if you’re still confident that you have a surplus, consider moving this amount to savings.

If you have a deficit, don’t panic! It can be easy to lose hope and panic if your budget has resulted in a deficit. However, take comfort in the fact that you now know and you can do something about it. If you hadn’t worked on your budget, you could quite easily have run out of money before your next pay cheque.

Step 8 – Moving from Deficit to a Balanced Budget

There are two possible options: make more money or cut your expenses.

The quickest option is to review your expenditure and look for items that you can reduce or cut out altogether. Obviously your committed expenditure, like rent, loan repayments, utilities etc cannot be cut (at least in the short term), but everything else is fair game.

Look at reducing your groceries, entertainment/fun money, travel costs, eating out, gift buying, clothes purchases etc. Be strong and get culling until you can, as a minimum, get your expenditure to match your income.

Believe me when I say, I know this can be hard, but the pain of going without is far less than the pain of wondering whether your card will pay or decline at the check-out!

Some Pitfalls To Look Out For

Don’t forget credit cards for invisible transactions

If you’re currently supporting your month-to-month expenditure with credit card purchases, make a note of how much you’re charging to your card each month. Supplementing your expenditure by using credit cards can make you feel richer than you actually are and in the long term will stretch your true budget to breaking point as your repayments gradually increase. Work each month to avoid using your credit card unless it’s well under control.

Surprise Expenditure and Emergencies

• Have you signed up for a magazine subscription which charges you annually?

• Is your car due for a service or MOT?

• How often do you get your hair cut?

These are all examples of expenditure which can surprise us by creeping up unexpectedly. Of course, we know it’s due…eventually, but it somehow comes as a surprise when it actually arrives. Do you need to plan any of these (or other stuff) into your budget?

Personal Budget Tips

Take your time and don’t stress!

If you want personal budgeting to work, you’ll need to be in it for the long haul, so take your time and don’t stress over the detail too much. Remember, if you haven’t previously budgeted, taking these steps will be a vast improvement!

Don’t overestimate income

This is so easy to do. For example if you do overtime, you might budget to receive overtime in the next month. But what would happen to your budget if you didn’t get the overtime you were relying on? In accounting-speak, ‘be prudent’. If it’s not 99.999% a given, don’t count on it. If it turns up, it’s a bonus and ready to use for next month.

Don’t underestimate expenditure

Budgeting can open our eyes to how much we really spend, which can make us to feel guilty, annoyed or even stupid…and that can lead us to make sudden, drastic changes. But, for change to stick, it needs to be doable and not feel like a punishment.

Forgive yourself for all that has gone before and move on from today. Set a reasonable expenditure budget, one that you feel comfortable you can stick with and congratulate yourself every day for sticking with your new plan.

Your New Shiny Budget

I hope that this article and the Basic Budget Worksheet will help you with your personal budgeting. Please let me know if you have any questions, you can leave a comment or email me. I’d love to hear how you get on with my ‘How to set up a personal budget’ guide! Happy budgeting and good luck!

Love how you called credit card surprises invisible transactions, as that is truly what they are & so easily forgotten.

Great post Nicola! I’ve been reading a book called “The Authentic Budget,” which goes through a little bit different process, but it’s been a great way for me to set up some saving and spending goals. I’ll write a review of it on my blog The Erica Upgrade Project once I’m done.